Welcome, Ka-Optimalliving!

Have you ever wondered why saving money or sticking to a budget can feel so difficult, even when you know it’s important? The truth is, achieving financial freedom isn’t just about numbers—it’s about finding your “why” and building habits that last. Let’s explore how simple goal setting for financial freedom can transform your family’s future, one step at a time.

H2: Introduction

Long-term financial security for your family doesn’t require complicated strategies. What matters most is consistency and a clear sense of purpose. Many people understand the value of saving, but without defined goals and emotional motivation, it’s easy to lose focus. Research shows that goal setting, habit formation, and emotional motivation are key drivers of financial well-being. [Finding Yo…amily Life | Word]

H2: Why Emotional Motivation Matters

Financial plans often fail not because of market changes, but because of lapses in human behaviour. Anchoring your plan to a powerful emotional purpose—your “why”—is essential. According to the American Psychological Association, connecting goals to personal values increases motivation and persistence. [Finding Yo…amily Life | Word]

- Define Your Emotional Why: Identify the feelings you want to achieve, such as “freedom from financial stress,” “peace of mind,” or “my children have choices.”

- Visualise Success: Use a financial vision board to make your goals tangible and keep them top of mind. [Finding Yo…amily Life | Word]

- Involve the Whole Family: Set family goals through open communication about shared values and dreams.

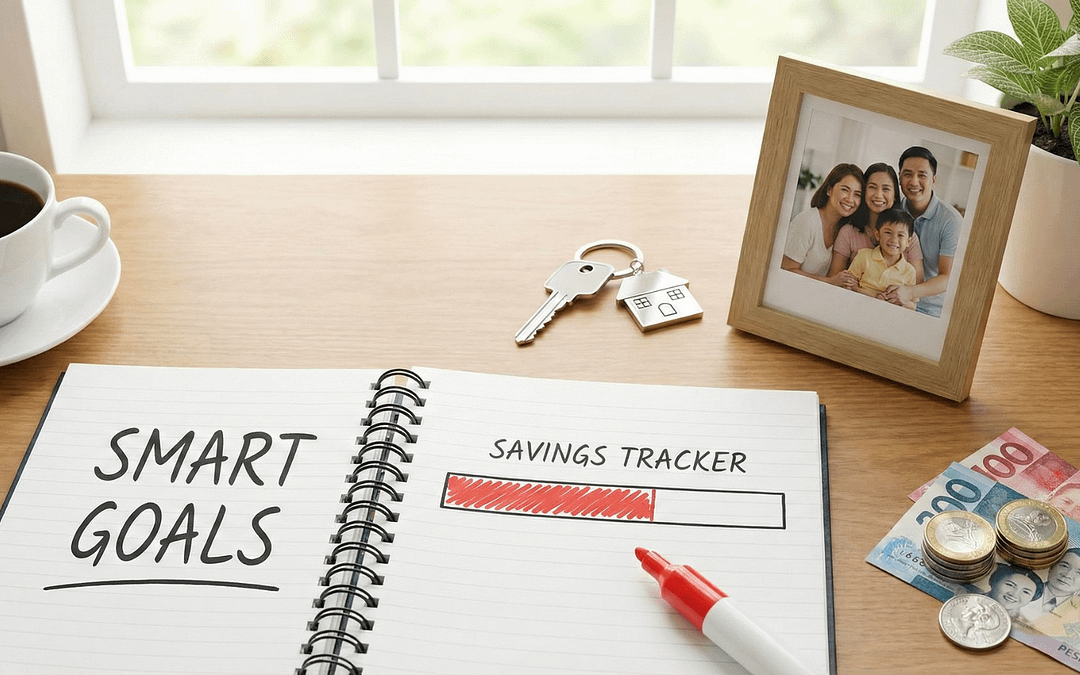

H2: Step 1: The Clarity Blueprint – Setting SMART Objectives

The SMART framework—Specific, Measurable, Achievable, Relevant, and Time-bound—is a proven tool for turning abstract financial desires into concrete objectives. [Finding Yo…amily Life | Word]

H3: Make Goals Specific and Measurable

Instead of “save money,” aim for “Save ₱10,000 in 6 months for an emergency fund.” Breaking down large goals into measurable milestones is critical for progress.

H3: Ensure Attainability and Set a Deadline

Goals must be achievable based on your income and time-bound with a firm deadline. This keeps you focused and accountable.

H3: Use Visual Trackers

Savings thermometers or charts provide visible evidence that small contributions add up. Seeing your progress can boost motivation and help you stay on track.

H2: Step 2: From Willpower to Automation – Stacking Good Habits

Sustainable wealth building relies on transforming daily routines into supportive financial systems. Behavioural science shows that habit stacking—pairing a new practice with an established habit—improves consistency. [Finding Yo…amily Life | Word]

H3: Integrate Financial Practices

For example, “After I make my morning coffee, I will check my bank account.” Linking new habits to existing routines makes them easier to remember.

H3: Automate Consistency

Set up automatic transfers for savings and investments right after your paycheck deposits. Automation removes the need for willpower and ensures you stay consistent.

H3: Plan for Weakness with WOOP

The WOOP framework (Wish, Outcome, Obstacle, Plan) helps create concrete “if-then” scripts to overcome obstacles. For example, “If I’m tempted to spend my savings, then I’ll review my vision board.” [Finding Yo…amily Life | Word]

H2: Step 3: Tackling Debt – Avalanche for Savings or Snowball for Motivation

Paying down high-interest debt is a critical priority. The best method depends on which strategy sustains your motivation.

H3: Debt Avalanche Method

Prioritise the debt with the highest interest rate first to save the most money overall. This method is efficient and reduces the total interest paid. [Finding Yo…amily Life | Word]

H3: Debt Snowball Method

Prioritise paying off the smallest debt balance first for rapid, visible wins. This approach can boost motivation and help you build momentum. [Finding Yo…amily Life | Word]

H2: Benefits of Simple Goal Setting

- Improved financial clarity and control

- Increased motivation and consistency

- Reduced financial stress

- Stronger family communication and shared purpose

H2: Frequently Asked Questions about Simple Goal Setting for Financial Freedom

Q1: What is the SMART goal framework?

SMART stands for Specific, Measurable, Achievable, Relevant, and Time-bound. It’s a proven way to make your financial goals clear and actionable.

Q2: How do I find my “why” for saving money?

Reflect on what matters most to you—security, freedom, opportunities for your children—and use these values to guide your goals.

Q3: What if I struggle to stick to my goals?

Try habit stacking and automation. Pair new habits with existing routines and set up automatic transfers to make saving effortless.

Q4: Which debt repayment method is best?

The avalanche method saves more money, while the snowball method offers quick wins. Choose the one that keeps you motivated.

Q5: When should I seek professional advice?

If you face complex financial decisions or persistent stress, consult a qualified financial adviser or mental health professional.

H2: Conclusion

Achieving long-term financial security is all about consistent, sound financial behaviour supported by clear systems. Start today by defining your goals with clarity using the SMART framework and reinforce them with your emotional “why.” Remember, small steps taken consistently can lead to big changes for your family’s future.

Ready to take the next step? Visit https://home.optimallivingph.store for practical tools and products to support your journey to financial freedom and a better family life.

References

- https://www.apa.org/monitor/2018/01/ce-corner-goals

- https://www.mayoclinic.org/healthy-lifestyle/adult-health/in-depth/habits/art-20046311

- https://www.psychologytoday.com/gb/blog/the-path-passionate-happiness/201812/vision-boards-and-the-science-goal-setting

- https://www.mindtools.com/a4wo118/smart-goals

- https://woopmylife.org/en/home

- https://www.consumerfinance.gov/ask-cfpb/what-is-the-debt-avalanche-method-en-2031/

- https://www.consumerfinance.gov/ask-cfpb/what-is-the-debt-snowball-method-en-2030/

Medical Disclaimer

“Medical Disclaimer: I am not a doctor. No material on this site is intended to be a substitute for professional medical advice, diagnosis, or treatment. Always seek the advice of your physician or other qualified healthcare provider regarding any medical condition or treatment and before undertaking a new health care regimen or wellness routine. Optimal Living PH does not recommend or endorse any specific tests, physicians, procedures, opinions, or other information that may be mentioned on this website. Reliance on any information provided by Optimal Living PH is solely at your own risk.”

Explore Our Favourite Wellness Tools

To help support your family’s overall well-being, we share tools and products that we believe in. If you are looking for practical tools to help you achieve a healthier lifestyle, check out our selection at the